March 1, 2023

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

The Portfolio Manager Commentary is provided by Trustmark’s Tailored Wealth Investment Management team. The opinions and analysis presented are accurate to the best of our knowledge and are based on information and sources that we consider to be reliable and appropriate for due consideration1.

Economic Outlook

U.S. Consumer Spending was up 1.8% for January, after having been down 0.1% in December. Personal Income was up 0.6% in January after having been up 0.3% in December. New single-family home sales came in at a 670,000 annualized rate for January versus 625,000 for December, both below long-term trend levels, which should be in the 800,000’s. The NAHB Housing Market Index came in at 42.0 for February, up from 35.0 for January but still below the neutral level of 50.0. Durable Goods Orders for January were down 4.5% for January versus +5.5% for December. The Chicago Business Barometer came in at 43.6 for February versus 44.3 for January, both levels being contractionary. U.S. Industrial Production came in flat for January after having been down 1.0% in December, with Capacity Utilization also flat at 78.3%. The Index of Leading U.S. Economic Indicators was -0.3% in January versus -0.8% in December. Finally, U.S. Producer Prices were up 0.7% in January versus -0.20% in December, with overall prices up 6.0% for the twelve months ended January 2023.

Fixed Income

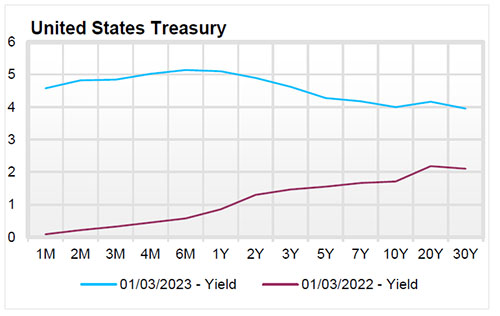

The U.S. Treasury Yield Curve remains inverted, with the 10-year yield trading at 3.93%, 88 basis points below the 2-year yield of 4.81%. Short-term rates have now breached 5.00% for both 6-month and 12-month Treasury Bills. At the most recent Federal Reserve Open Market Committee meeting ended February 1st, the Federal Funds Rate range was increased by 0.25%, to 4.50% to 4.75%. In terms of commentary, the FOMC said “the Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time.” The FOMC also said that “In determining the extent of future increases in the target range, the Committee will take into account…….the lags with which monetary policy affects economic activity and inflation.” Finally, the FOMC reiterated that “the Committee is strongly committed to return inflation to its 2% objective.” The next FOMC meeting is in late March.

Yield Curve

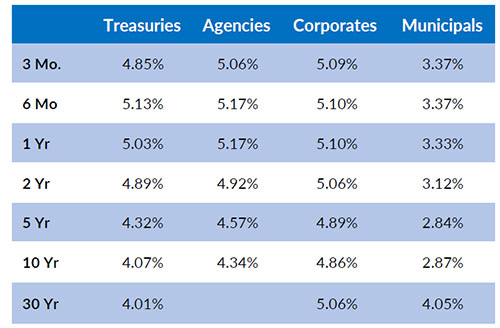

Current Generic Bond Yields

Equity

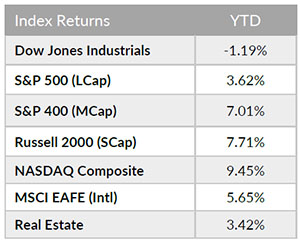

US Equity finished February down though the S&P 500 index is still up 3.62% year-to-date and up ~11% above its October lows. All eyes continue to be on the Fed as the repricing of the Fed’s rate hike continues to ring in the headlines. The month began with an expected 25bps hike and later turned to mentions of a 50bps hike, though consensus still seems to see a 25bps hike. The back-and-forth narrative seems to be due to the disinflation theme gathering momentum, however, several releases, such as January’s PPI and Core PCE, showed that there could still be work needed from the Fed (or specifically supporting the higher for longer theme).

Cyclical sectors continue to lead the market as Communication Services (+11.48%) and Consumer Discretionary (+12.68%) outperform the more defensive natured sectors such as Utilities (-7.80%) and Energy (-4.32%). Value and Growth are a wash with returns of 3.73% and 3.52% respectively. The S&P 500 closed at 3970 month end.

{"dialogBean":{"articleAbstract":"U.S. Consumer Spending was up 1.8% for January, after having been down 0.1% in December. Personal Income was up 0.6% in January.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"March 01, 2023","trustmarkExpirationDate":"July 26, 2026","authorBean":{"authorName":"Grant Melancon","profilePicPath":"/content/dam/trustmark/authors/author-Grant-Melancon.jpg"}},"pageTitle":"Portfolio Manager Commentary - March 1, 2023","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investments"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2023/3/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2023/3/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

January 15, 2023

The S&P Manufacturing Purchasing Managers Index came in at 46.7 for December.

February 1, 2023

The Index of Leading Economic Indicators was down 1.0% in December, following a 1.0% move down in November.

February 15, 2023

The ISM Manufacturing Index was 47.4 for January vs. 48.4 for December, while the S&P Purchasing Managers Index was 46.9 for January versus 46.8 for December.