November 15, 2025

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In October, the ISM Services PMI registered 52.4, indicating modest expansion in the services sector. The NFIB Small Business Optimism Index increased to 98.2, with small business owners identifying labor quality as the most important problem they face. Due to a lack of data collection during the recent federal government shutdown, the Bureau of Labor Statistics has indicated that employment data, consumer price, and producer price data for the month of October are at risk of not being published. The ADP Employment Report showed that the private sector added 42,000 jobs in October, while average hourly earnings increased 4.5% from a year ago. The University of Michigan’s Consumer Sentiment Index posted a preliminary November reading of 50.3, now at the lowest level since June 2022. The average interest rate for a 30-year fixed rate mortgage was approximately 6.24% as of November 7.

Fixed Income

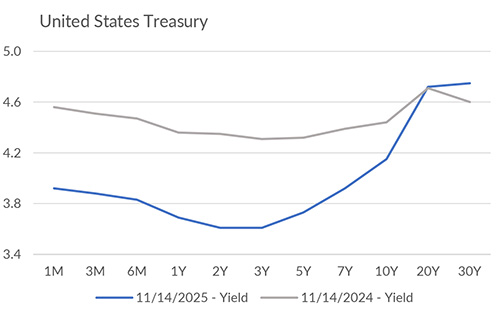

The federal funds target range remains 3.75%–4.00% following a 25 bp cut last month. Futures markets assign roughly a 40% probability of an additional 25 bp rate cut at the upcoming December meeting. Despite recent policy easing, long-duration Treasury yields remain elevated. The 10-year yield closed at 4.15% last Friday, while the 30-year reached roughly 4.75%. Credit markets remain broadly stable with investment-grade bonds near record low risk premiums. The ICE BofA U.S. High Yield Index indicates a spread of only 3.07% for bonds rated BB and below. Meanwhile, the ICE BofA CCC & Lower US High Yield Index shows a current spread of 9.02% for bonds rated CCC or below, with a slight trend higher in recent weeks.

Yield Curve

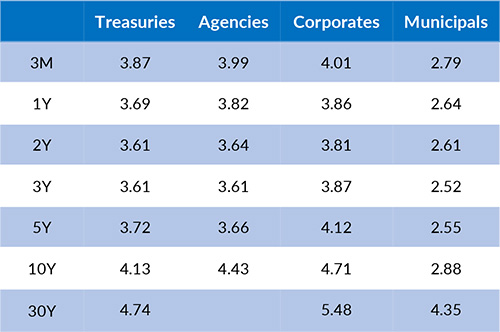

Current Generic Bond Yields

Equities

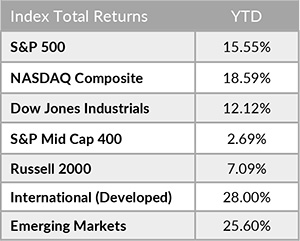

Since the start of 2025, equities have produced strong returns, with international markets generally outperforming U.S. markets. During most of the year, cyclical sectors like Technology and Communications Services have led the market to new all-time highs. However, defensive sectors like Health Care, Energy, and Consumer Staples have outperformed since the start of November. As the Q3 earnings season continues to wind down, S&P 500 companies continue to report strong results. With 92% of companies having reported, the index is on track to report its highest blended net profit margin in over 15 years.

In 2025, the best performing U.S. sectors have been Information Technology (+25.09%), Communication Services (+23.62%), and Utilities (+19.77%). The worst performing sectors have been Consumer Staples (+2.95%), Real Estate (+3.07%), and Consumer Discretionary (+3.26%). On a total return basis, the Russell 1000 Growth Index has returned 17.83% year to date, while the Russell 1000 Value Index has increased 12.26% over the same period.

{"dialogBean":{"articleAbstract":"In October, the ISM Services PMI registered 52.4, indicating modest expansion in the services sector.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"November 15, 2025","trustmarkExpirationDate":"July 27, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - November 15, 2025","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2025/11/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2025/11/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

November 1, 2025

The Atlanta Federal Reserve projects an annualized real GDP growth rate of 4.0% for Q3 2025.

October 15, 2025

In September, the ISM Services PMI registered at 50.0, indicating neutral levels of service sector activity.