December 1, 2025

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

The Atlanta Federal Reserve currently estimates real GDP growth of 3.9% for Q4 2025, pointing towards continued resilience in overall economic activity. The ISM Manufacturing PMI registered 48.2 in November, reflecting a mild contraction in the manufacturing sector. Consumer sentiment fell modestly, with the University of Michigan Index posting a final November reading of 51, down from 53.6 in October. Using the latest data from September, the Consumer Price Index increased 3.0% year-over-year. Over the same period, the Producer Price Index increased 2.7%. Forward inflation expectations are at a twelve-month low as the 5-year breakeven inflation rate is approximately 2.29%. The NAHB Housing Market Index rose to 38 in November, its highest level in seven months. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.23% as of November 21.

Fixed Income

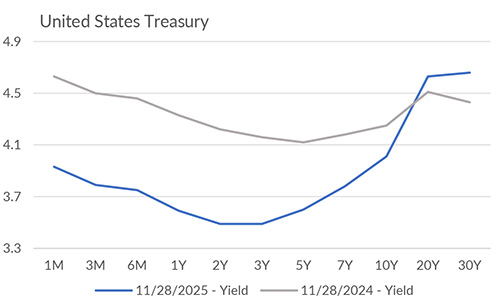

The Federal Reserve’s target range is 3.75%–4.00%, following two consecutive 25 bps rate cuts in September and October. Futures markets imply an 85% probability of another 25 bps cut at the December 9–10 FOMC meeting, though some policymakers have adopted a more cautious tone as economic data releases continue to be delayed. Despite the Fed’s easing posture, Treasury yields rose on the long end of the curve in November with the 30-year Treasury yield approaching its highest level over the past three months. The 10-year yield was nearly unchanged month-over-month. Bond market volatility was sporadic over the past month, with the ICE BofA MOVE Index up 25% over a three-week period, before closing the month up just 3%.

Yield Curve

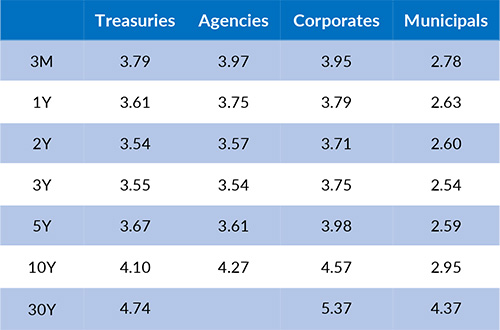

Current Generic Bond Yields

Equities

The S&P 500 experienced a 5% drawdown during the month of November. However, the index still managed to close the month near all-time highs. Market leadership broadened modestly as several defensive sectors including Materials, Consumer Staples, and Health Care outperformed amid a modest pullback in some large-cap technology names. Individual investor sentiment has shifted negative over the past month, with the AAII survey showing only 32% of respondents identifying as bullish for the week ending November 27. As we enter the final month of the year, a clear divergence of returns amongst the S&P 500 constituents has continued. So far in 2025, around 32% of the individual stocks in the S&P 500 are underperforming the index by 20% or more. Meanwhile, only 15% of the stocks in the index are outperforming by 20% or more.

In 2025, the best performing U.S. sectors have been Communication Services (+34.88%), Information Technology (+24.36%), and Utilities (+22.30%). The worst performing sectors have been Real Estate (+4.86%), Consumer Discretionary (+5.22%), and Consumer Staples (+5.57%), On a total return basis, the Russell 1000 Growth Index has returned 19.30% year to date, while the Russell 1000 Value Index has increased 15.13% over the same period.

{"dialogBean":{"articleAbstract":"The Atlanta Federal Reserve currently estimates real GDP growth of 3.9% for Q4 2025, pointing towards continued resilience in overall economic activity.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"December 01, 2025","trustmarkExpirationDate":"July 28, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - December 1, 2025","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2025/12/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2025/12/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

November 15, 2025

In October, the ISM Services PMI registered 52.4, indicating modest expansion in the services sector.

November 1, 2025

The Atlanta Federal Reserve projects an annualized real GDP growth rate of 4.0% for Q3 2025.

October 15, 2025

In September, the ISM Services PMI registered at 50.0, indicating neutral levels of service sector activity.