January 1, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q4 2025. The ISM Manufacturing PMI registered 47.9 in December, falling slightly for the third consecutive month. The University of Michigan Consumer Sentiment Index posted a final December reading of 52.9, remaining near the lowest levels in the survey’s history. The Consumer Price Index increased 2.7% year-over-year in November, while the Producer Price Index also rose by 2.7% over the same period. Forward inflation expectations remain muted, with the 5-year breakeven inflation rate at approximately 2.28%. The NAHB Housing Market Index rose to 39 in November, continuing a steady move higher. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.31% as of December 19.

Fixed Income

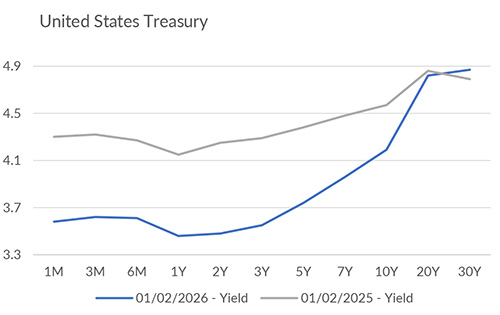

The U.S. fixed income market in 2025 was shaped by the Federal Reserve’s rate-cutting cycle, which delivered three 25-bps cuts, bringing the fed funds target range to 3.50–3.75% by year-end. Treasury yields generally declined over the course of the year, with the 10-year yield ending December near 4.17% and the 2-year yield closing near 3.48%. Credit markets remained resilient, as investment-grade spreads tightened to around 1.75%, placing them in the 15th percentile of values since 2000. Notably, the Bloomberg U.S. Aggregate Bond Index returned approximately +7.2%, its strongest annual performance since 2020.

Yield Curve

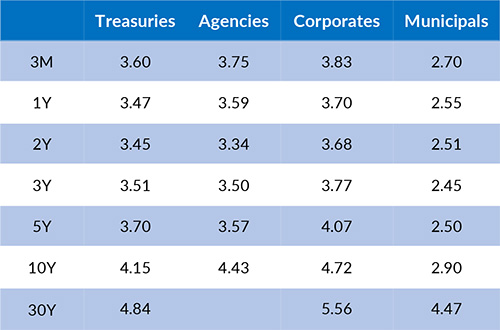

Current Generic Bond Yields

Equities

In 2025, the U.S. equity market extended the bull run that began in late 2022, with the S&P 500 gaining 17.9%, the Nasdaq advancing by 21.1%, and the Dow up 14.7%. The year featured a sharp midyear correction triggered by unexpected tariff measures, briefly erasing trillions in market value before a swift recovery. Artificial intelligence dominated the narrative, as technology and data infrastructure themes outperformed while defensive sectors lagged. Earnings growth reflected this divide as “Magnificent 7” earnings are projected to grow by 22.3% for the calendar year 2025, compared to 9.4% for the other 493 companies. Volatility (VIX) ended the year at its lowest level of 2025, and S&P 500 valuations stayed nearly the same from January 1 to year-end, setting a steady backdrop as markets enter 2026.

In 2025, the best performing U.S. sectors were Communication Services (+33.55%), Information Technology (+24.04%), and Industrials (+19.42%). The worst performing sectors were Real Estate (+2.70%), Consumer Staples (+3.90%), and Consumer Discretionary (+6.04%). On a total return basis, the Russell 1000 Growth Index returned 18.56%, while the Russell 1000 Value Index increased 15.91% over the same period.

{"dialogBean":{"articleAbstract":"The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q4 2025.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"January 01, 2026","trustmarkExpirationDate":"July 26, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - January 1, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/1/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/1/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

December 15, 2025

In November, the ISM Services PMI registered 52.6, indicating the strongest growth in the services sector in nine months.

December 1, 2025

The Atlanta Federal Reserve currently estimates real GDP growth of 3.9% for Q4 2025, pointing towards continued resilience in overall economic activity.

November 15, 2025

In October, the ISM Services PMI registered 52.4, indicating modest expansion in the services sector.