January 15, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In December, the ISM Services PMI registered 54.4, the highest reading in over a year. The NFIB Small Business Optimism Index rose to 99.5, remaining above its long-run average and marking a second consecutive monthly increase. Consumer sentiment improved modestly, with the University of Michigan Consumer Sentiment Index rising to 54.0 in January. Labor market data showed the U.S. added 50,000 jobs in December, missing expectations. Meanwhile, the unemployment rate improved slightly to 4.4% over the same period. The Consumer Price Index rose 0.3% month-over-month, with consumer prices up 2.7% annually. The Producer Price Index rose 0.2% month-over-month, with producer prices up 3.0% from a year ago. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.18% as of January 9.

Fixed Income

The federal funds target range remains 3.50%–3.75%, with the next FOMC meeting scheduled for January 28. In the short term, the FOMC Board is expected to hold rates during the January meeting. Looking ahead, FOMC participants have a wide range of expectations regarding year-end rate targets. Some voters see an appropriate policy set at a range as high as 3.75%-4.00%, while others expect to lower rates below 3.0%. Mortgage rate spreads made headlines this week as potential mortgage bond purchases by Fannie Mae and Freddie Mac may provide support for tighter spreads. Mortgage rate spreads as measured by the difference between the 30-year fixed-rate mortgage average and the 10-year Treasury yield made a 35 year high of 3.1% in 2023. Since then, mortgage rate spreads have fallen steadily and recently dropped below 2%.

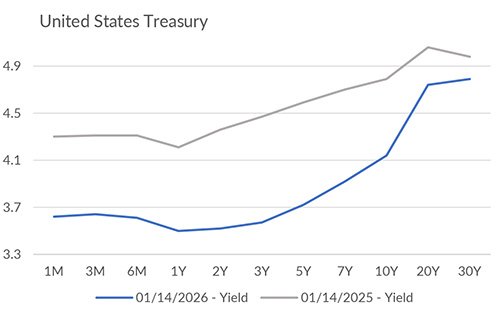

Yield Curve

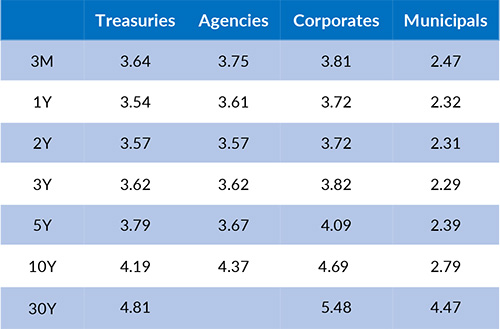

Current Generic Bond Yields

Equities

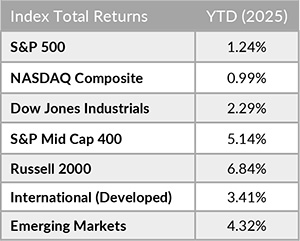

As of January 14, the S&P 500 closed at 6,926.60 and is up 1.2% year-to-date. Meanwhile, small-cap stocks have led early with the Russell 2000 up 6.8% year-to-date. Corporate demand remains a solid pillar of support, as S&P 500 buybacks totaled $249B in Q3 2025. Buybacks for the trailing 12-month period ending September 2025 surpassed $1T. Notably, the share of overall stock buybacks was dominated by the largest companies in the index. The 20 largest S&P 500 companies accounted for 49.5% of buybacks during Q3 2025. International equities continue to show strong trailing performance, with MSCI reporting 12-month returns of 36.5% for International Developed stocks and 42.9% for the Emerging Markets stocks.

In 2026, the best performing U.S. sectors are Energy (+7.54%), Materials (+7.37%), and Industrials (+5.91%). The worst performing sectors are Financials (-1.15%), Information Technology (-1.14%), and Utilities (+1.14%). On a total return basis, the Russell 1000 Growth Index returned -0.69%, while the Russell 1000 Value Index increased 3.82% over the same period.

{"dialogBean":{"articleAbstract":"In December, the ISM Services PMI registered 54.4, the highest reading in over a year.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"January 15, 2026","trustmarkExpirationDate":"July 28, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - January 15, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/1/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/1/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

January 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q4 2025.

December 15, 2025

In November, the ISM Services PMI registered 52.6, indicating the strongest growth in the services sector in nine months.

December 1, 2025

The Atlanta Federal Reserve currently estimates real GDP growth of 3.9% for Q4 2025, pointing towards continued resilience in overall economic activity.