February 1, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

The Atlanta Federal Reserve currently estimates real GDP growth of 4.2% for Q4 2025. After a notable delay in previous releases, the U.S. Leading Economic Index declined again in October and November, with the index now contracting modestly since March 2025. The ISM Manufacturing PMI registered 52.6 in January, marking a large, unexpected increase in manufacturing sector activity. However, the chair of the ISM Manufacturing Business Survey Committee noted that the increase is largely due to companies reordering after the holidays and attempts to front-run ongoing tariff impacts. Consumer sentiment remains historically low, with the University of Michigan Consumer Sentiment Index reaching 56.4 in January. Consumer sentiment has improved modestly over the past two months and sits at its highest level since August 2025. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.24% as of January 23, breaking three consecutive weeks of lower rates.

Fixed Income

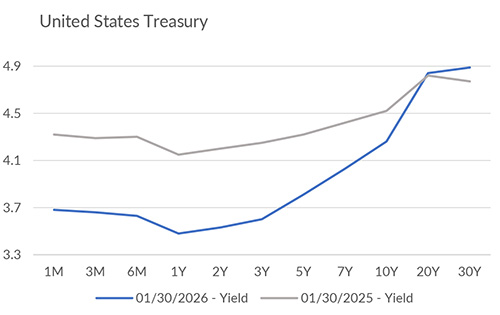

The Federal Open Market Committee met last week and voted to keep its overnight rate unchanged at 3.50%-3.75%. The CME FedWatch Tool indicates that futures markets are pricing in approximately two rate cuts by the end of the year. Bond markets are signaling that the easing cycle is likely to be shallower and more uneven than previously expected. Since the October 2025 FOMC meeting, the 10-year Treasury yield has risen by nearly 30 bps, even as short-end rates have stabilized. Treasury supply remains a dominant theme in 2026. Net marketable borrowing by the Treasury Department is projected to exceed $2 trillion in FY2026, likely keeping some upward pressure on intermediate and long-dated yields despite policy easing. Looking ahead, the next FOMC meeting is scheduled for March 17-18, 2026. President Donald Trump chose Kevin Warsh, who served as a governor on the central bank's board from 2006 to 2011, as head of the Federal Reserve. Warsh is set to take over as the next Federal Reserve Chair in May 2026.

Yield Curve

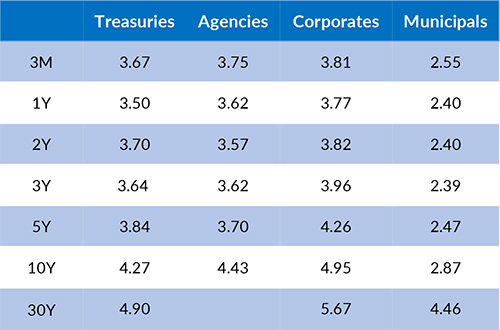

Current Generic Bond Yields

Equities

Equity markets have begun 2026 with leadership and positioning dynamics that appear materially different from last year. Through January, small-cap stocks and several defensive sectors have outperformed the S&P 500 index thus far. The S&P 500 posted its best month since October, and the NASDAQ broke two consecutive monthly declines. We are currently in the midst of Q4 earnings season, and with 33% of S&P 500 companies having reported, the blended earnings growth rate is currently 11.9%.

In 2026, the best performing U.S. sectors have been Energy (+14.43%), Materials (+8.71%), and Consumer Staples (+7.71%). The worst performing sectors have been Financials (-2.41%), Information Technology (-1.66%), and Health Care (-0.02%). On a total return basis, the Russell 1000 Growth Index returned -1.51%, while the Russell 1000 Value Index increased 4.56% over the same period.

{"dialogBean":{"articleAbstract":"The Atlanta Federal Reserve currently estimates real GDP growth of 4.2% for Q4 2025.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"February 01, 2026","trustmarkExpirationDate":"June 19, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - February 1, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/2/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/2/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

January 15, 2026

In December, the ISM Services PMI registered 54.4, the highest reading in over a year.

January 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q4 2025.

December 15, 2025

In November, the ISM Services PMI registered 52.6, indicating the strongest growth in the services sector in nine months.