February 15, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In January, the ISM Services PMI registered 53.8, beating expectations and signaling continued expansion in the services sector. The NFIB Small Business Optimism Index fell slightly to 99.3, remaining near its long-run average. In the NFIB survey, small business owners most frequently cited labor quality and the cost or availability of insurance as their top concerns. Labor market conditions remained resilient, with non-farm payrolls increasing by 130,000 in January, well above forecasts of 70,000. The unemployment rate fell to 4.3%, the lowest level since August 2025. Average hourly earnings rose 3.7% year-over-year, the slowest pace since July 2024. Inflation continues to show signs of cooling, with the Consumer Price Index rising just 2.4% year-over-year in January. Consumer sentiment continues to improve modestly, with the University of Michigan Index posting a preliminary February reading of 57.3. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.21% as of February 6.

Fixed Income

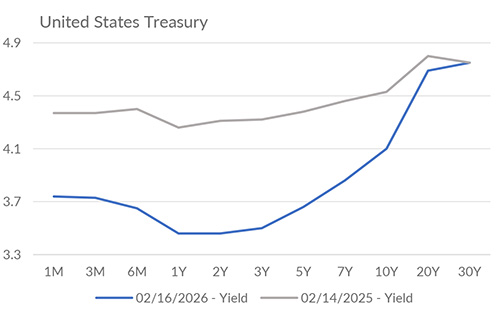

The federal funds target range remains at 3.50%–3.75%, with the next FOMC meeting scheduled for March 17–18. Treasury yields have moved notably lower since the beginning of February. The 2-year Treasury yield has moved from 3.57% to 3.44% in the past two weeks. Meanwhile, the 10-year Treasury yield has moved from 4.28% to 4.06% over the same period. Credit spreads remain narrow, with Investment Grade Bond yields (Moody’s) relative to the 10-Year Treasury yield at around 1.66%. The spread for High-Yield Bonds (BofA) remains tight at about 2.41%, consistent with low default expectations. Overall, falling Treasury yields alongside narrow credit spreads suggest markets are pricing easing inflation pressures without signaling meaningful deterioration in economic or credit fundamentals.

Yield Curve

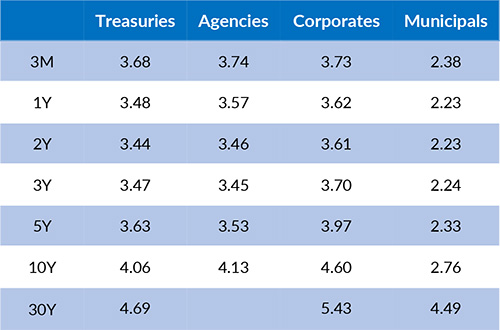

Current Generic Bond Yields

Equities

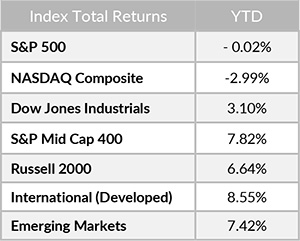

The S&P 500 Index and the NASDAQ Composite have declined for two consecutive weeks. Equity markets have faced continued pressure from AI stocks and their implications for software and related business models. While headline indices weakened, breadth was comparatively better, as the equal-weight S&P 500 finished last week slightly positive. Small-cap stocks continue to outperform this year, currently up 6.64% in 2026. S&P 500 earnings for Q4 2025 have beaten expectations thus far. With 74% of companies having reported, the blended year-over-year earnings growth rate for Q4 2025 is 13.2%, versus previous expectations of 8.3%. Additionally, revenue is growing at the highest rate in three years, with ten of eleven sectors reporting year-over-year growth.

In 2026, the best performing U.S. sectors have been Energy (+21.78%), Materials (+16.64%), and Consumer Staples (+15.83%). The worst performing sectors have been Financials (-5.65%), Consumer Discretionary (-4.94%), and Information Technology (-4.90%). On a total return basis, the Russell 1000 Growth Index returned -5.45%, while the Russell 1000 Value Index increased 6.42% over the same period.

{"dialogBean":{"articleAbstract":"In January, the ISM Services PMI registered 53.8, beating expectations and signaling continued expansion in the services sector.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"February 15, 2026","trustmarkExpirationDate":"July 27, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - February 15, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/2/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/2/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

February 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 4.2% for Q4 2025.

January 15, 2026

In December, the ISM Services PMI registered 54.4, the highest reading in over a year.

January 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q4 2025.