March 15, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In February, the ISM Services PMI registered 56.1, indicating the fastest growth in the services sector since August 2022. The NFIB Small Business Optimism Index slipped to 98.8, though it remained slightly above its long-run average. Labor market conditions softened in February, with nonfarm payroll employment falling by 92,000 while the unemployment rate held at 4.4%. Average hourly earnings rose 3.8% year-over-year. Inflation remained contained, with the Consumer Price Index up just 2.4% from a year ago. Consumer sentiment weakened, with the University of Michigan index posting a preliminary March reading of 55.5, still well below the long-run average of 84.6. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.11% as of March 12.

Fixed Income

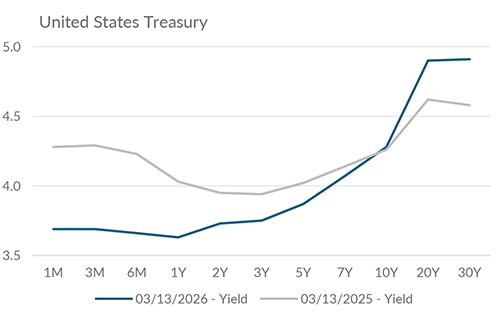

The federal funds target range remains at 3.50%–3.75%, while the next FOMC meeting is scheduled for March 17–18. Markets are expecting the Federal Reserve to leave rates unchanged this week. Treasury markets have become increasingly sensitive to geopolitical inflation risk, with oil prices near $100. The ICE BofA MOVE Index, which measures implied volatility across U.S. Treasury yields, is currently at its highest level in over six months. The 2-year Treasury yield recently moved above the effective federal funds rate for the first time since February 2025, reflecting shifting market expectations around the trajectory of monetary policy. Credit spreads have widened modestly in recent weeks, reflecting increased risk sensitivity rather than broad-based stress in credit markets.

Yield Curve

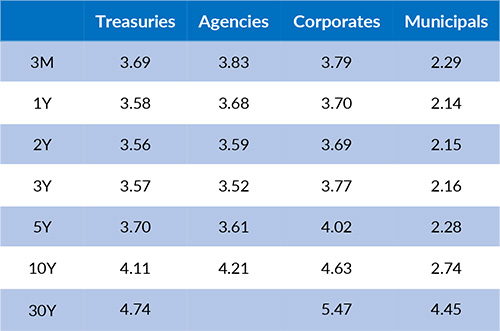

Current Generic Bond Yields

Equities

U.S. equities have experienced volatility in recent weeks, as rising oil prices and renewed inflation concerns have overshadowed an otherwise strong earnings season. For the week ended March 13, the S&P 500, Dow Jones, Nasdaq, and Russell 2000 all declined 1%-2%, and closed at or near their lowest levels of the year. Even so, underlying corporate results remain solid. The estimated year-over-year earnings growth rate for the S&P 500 in Q1 2026 stands at 11.4%. Current equity valuations reflect expectations for strong earnings growth with the forward 12-month price-to-earnings ratio for the S&P 500 at 20.7, slightly above the 10-year average of 19.3. Overall, equity performance in 2026 has exhibited significant dispersion across individual stocks and sectors, with recent volatility reflecting heightened macroeconomic uncertainty.

In 2026, the best performing U.S. sectors have been Energy (+29.21%), Consumer Staples (+10.48%), and Utilities (10.04%). The worst performing sectors have been Financials (-10.74%), Consumer Discretionary (-7.90%), and Information Technology (-6.62%). On a total return basis, the Russell 1000 Growth Index returned -7.33%, while the Russell 1000 Value Index increased 2.15% over the same period.

{"dialogBean":{"articleAbstract":"In February, the ISM Services PMI registered 56.1, indicating the fastest growth in the services sector since August 2022.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"March 15, 2026","trustmarkExpirationDate":"July 28, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - March 15, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/3/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/3/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

March 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q1 2026, suggesting continued underlying economic resilience.

February 15, 2026

In January, the ISM Services PMI registered 53.8, beating expectations and signaling continued expansion in the services sector.

February 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 4.2% for Q4 2025.