April 1, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

The Atlanta Federal Reserve currently estimates real GDP growth of 1.9% for Q1 2026, pointing to slower but still positive activity for the period. The U.S. Leading Economic Index declined 0.1% in January to 97.5, marking six consecutive monthly declines. The ISM Manufacturing PMI registered 52.7 in March, the highest reading since August 2022, indicating continued expansion in factory activity. The University of Michigan Consumer Sentiment Index posted a final March reading of 53.3, down from 56.6 in February. Producer prices increased 3.4% in February, well above expectations. Forward inflation expectations also edged higher, with the 5-year breakeven inflation rate at 2.54% as of March 31. Housing conditions remain subdued, with the NAHB Housing Market Index posting a reading of 38 in March, still well below a neutral reading of 50. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.57% as of March 27, rising sharply from a month ago.

Fixed Income

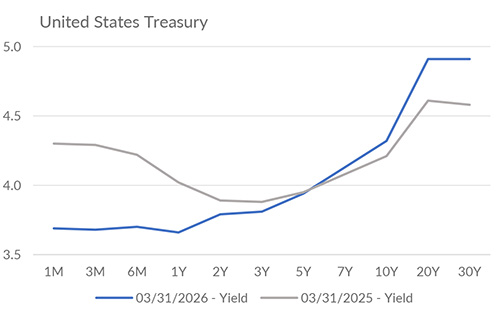

The Federal Reserve left the federal funds target range unchanged at 3.50%–3.75% at its March meeting. The committee projected just one 25 bp rate cut in 2026, while noting that uncertainty tied to Middle East developments had increased. Treasury yields across the curve shifted higher in March as the Iran conflict pushed oil prices sharply higher and sparked inflation concerns. The 10-year Treasury yield rose by nearly 50 bps from its February low before retreating in recent sessions. Credit spreads have widened only modestly and remain tight by historical standards. Investment-grade bond spreads have held up well, as Moody’s Baa bond yield relative to the 10-year Treasury rate stands at just 1.76%. The ICE BofA U.S. High Yield Index relative to the 10-year Treasury rate is currently 2.88%. Looking ahead, futures markets currently project that the federal funds target range will end the year at its current level.

Yield Curve

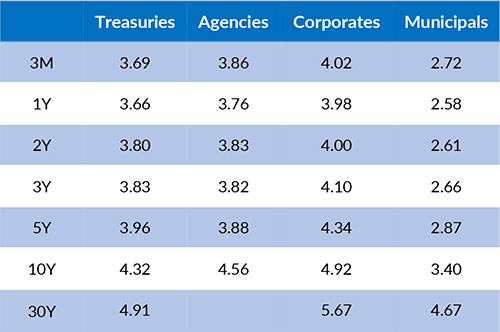

Current Generic Bond Yields

Equities

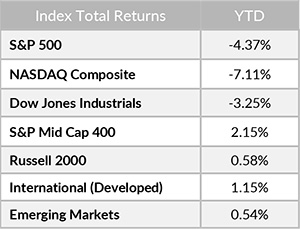

Equity markets have experienced heightened volatility amid the ongoing conflict in the Middle East. Recent sessions have been a great reminder that some of the market’s strongest single-day gains tend to occur near its weakest days. Even after a sharp relief rally on March 31, the S&P 500, Dow Jones, and NASDAQ still managed to post their worst quarterly performance since 2022. The conflict has exacerbated a sector leadership change that had been unfolding since the start of the year. Energy was the only S&P 500 sector to post gains in March, while 84% of S&P 500 stocks declined during the month.

In 2026, the best performing U.S. sectors have been Energy (+38.25%), Materials (+9.73%), and Utilities (+8.26%). The worst performing sectors have been Financials (-9.35%), Consumer Discretionary (-9.19%), and Information Technology (-9.13%). On a total return basis, the Russell 1000 Growth Index returned -9.78%, while the Russell 1000 Value Index increased 2.10% over the same period.

{"dialogBean":{"articleAbstract":"The Atlanta Federal Reserve currently estimates real GDP growth of 1.9% for Q1 2026, pointing to slower but still positive activity for the period.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"April 01, 2026","trustmarkExpirationDate":"May 26, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - April 1, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/4/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/4/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

March 15, 2026

In February, the ISM Services PMI registered 56.1, indicating the fastest growth in the services sector since August 2022.

March 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 3.0% for Q1 2026, suggesting continued underlying economic resilience.

February 15, 2026

In January, the ISM Services PMI registered 53.8, beating expectations and signaling continued expansion in the services sector.