May 15, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In April, the ISM Services PMI registered 51, rising from a 3-year low in March. The NFIB Small Business Optimism Index increased modestly to 95.9. A net 27% of small businesses plan to raise prices over the next 3 months. Labor market conditions remained stable in April, with non-farm payrolls increasing by 115,000 while the unemployment rate held at 4.3%. Average hourly earnings increased 3.6% year-over-year, continuing a gradual moderation in wage growth trends. The Consumer Price Index surged 3.8% year-over-year in April. Energy costs jumped 17.9% over the period. Meanwhile, the Producer Price Index rose 6.0% from a year ago, the largest change since December 2022. The University of Michigan Consumer Sentiment Index continues to make record lows, posting a preliminary May reading of 48.2. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.46% as of May 8.

Fixed Income

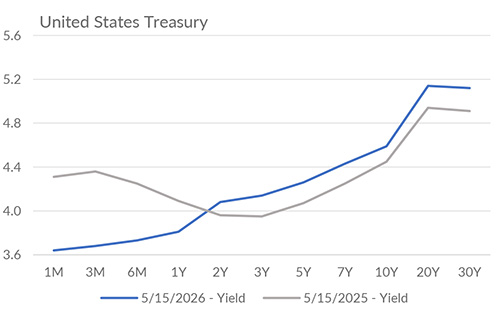

The federal funds target range remains at 3.50%–3.75% following the April FOMC meeting, where policymakers held rates steady and reiterated a data-dependent approach amid persistent inflation uncertainty. Notable increases in inflation data are keeping the Fed in a “hold” stance for now, eliminating expectations for any near-term rate cuts and maintaining pressure on the front end of the curve. Interest rate futures markets are pricing in roughly a 50% probability of at least one interest rate hike by the end of 2026. Long-duration Treasury yields have climbed higher in recent weeks. The 30-year Treasury yield recently reached its highest level since 2007. Despite tighter financial conditions, spreads on high-yield bonds remain near cycle lows.

Yield Curve

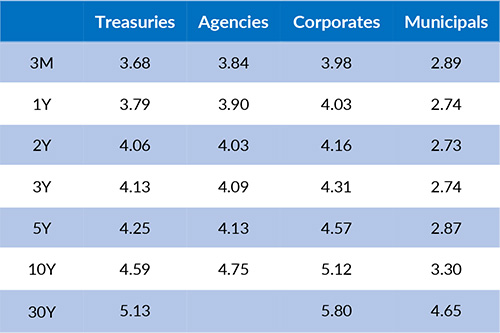

Current Generic Bond Yields

Equities

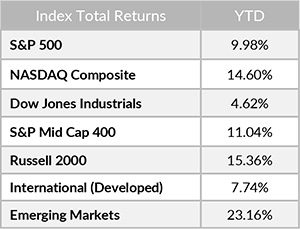

U.S. equities have continued to advance in May, with the S&P 500 reaching new all-time highs. Large-cap equity performance remains supported by a sharp rebound in technology stocks, while breadth indicators suggest participation remains somewhat narrow. From a valuation perspective, the S&P 500 currently trades at a trailing P/E ratio of 27.8, which is above both the five-year average of 24.1 and the ten-year average of 22.6. Using forward estimates, the index trades at a P/E ratio of 21.3, also above the five-year average of 20.2 and the ten-year average of 19.4. Meanwhile, earnings expectations continue to improve, with consensus estimates for S&P 500 earnings growth at 22.5% for calendar year 2026 as of May 15.

In 2026, the best performing U.S. sectors have been Energy (+33.81%), Information Technology (+22.58%), and Materials (+11.41%). The worst performing sectors have been Financials (-6.22%), Health Care (-5.88%), and Consumer Discretionary (-2.22%). On a total return basis, the Russell 1000 Growth Index has returned 4.26% year to date, while the Russell 1000 Value Index has increased 10.04% over the same period.

{"dialogBean":{"articleAbstract":"In April, the ISM Services PMI registered 51, rising from a 3-year low in March.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"May 15, 2026","trustmarkExpirationDate":"July 27, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - May 15, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/5/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/5/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

May 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of approximately 3.5% for Q2 2026, suggesting continued underlying economic resilience.

April 15, 2026

In March, the ISM Services PMI registered 54.0, indicating continued expansion in the services sector.

April 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of 1.9% for Q1 2026, pointing to slower but still positive activity for the period.