June 1, 2026

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

The Atlanta Federal Reserve currently estimates real GDP growth of approximately 3.0% for Q2 2026, suggesting continued economic resilience. The U.S. Leading Economic Index increased 0.1% in April and is nearly unchanged from the level at the end of 2025. The ISM Manufacturing PMI registered 54.0 in May, its highest reading since 2022, indicating continued expansion in factory activity. Forward inflation expectations have been volatile in recent weeks. The 5-Year Breakeven Inflation Rate was 2.52% at the end of May, falling 20 bps in 4 weeks. Labor market indicators remain mixed, with continuing jobless claims declining 6% since year-end 2025, while the labor force participation rate has fallen to a five-year low. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.53% as of May 29.

Fixed Income

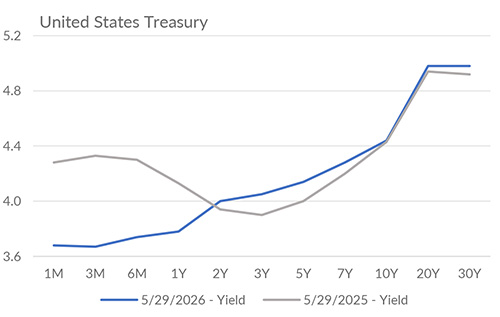

The federal funds target range remains at 3.50%-3.75%. Recent economic releases have reinforced the view that inflation remains the primary challenge of the FOMC’s dual mandate, leading markets to scale back expectations for near-term policy easing. Intermediate Treasury yields moved higher over the past month as markets continue to brace for a higher-for-longer interest rate environment. Foreign demand for U.S. Treasury securities remains a key market focus, as federal borrowing may lead to increasing pressure on long-term interest rates. The ICE BofA Bond MOVE Index, a measure of bond market volatility, rose over 20% in two sessions before ending the month nearly unchanged. Looking ahead, the next FOMC meeting is scheduled for June 16-17.

Yield Curve

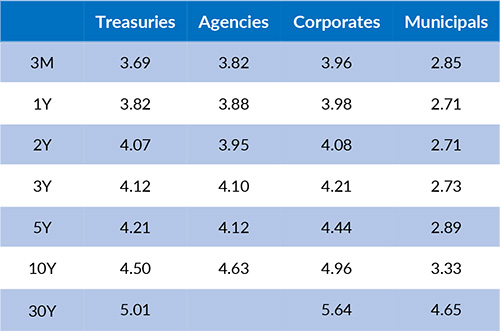

Current Generic Bond Yields

Equities

U.S. equity markets continued their advance in May, with the S&P 500 posting eleven all-time closing highs during the month. The index posted back-to-back months of 5% gains. Leadership remained concentrated in areas tied to artificial intelligence and digital infrastructure, with Information Technology advancing nearly 16% and accounting for the majority of the index’s monthly return. Outside the U.S., emerging market equities have outperformed the S&P 500 again in 2026, reinforcing the broader theme of expanding global market leadership. Despite record highs for the major indices, the current market is characterized by stock dispersion and low correlations, suggesting security selection is playing a larger role in performance than broad market direction.

In 2026, the best performing U.S. sectors have been Energy (+26.04%), Information Technology (+23.81%), and Materials (+11.94%). The worst performing sectors have been Financials (-5.32%), Health Care (-2.96%), and Consumer Discretionary (+4.11%). On a total return basis, the Russell 1000 Growth Index returned 13.68% year to date, while the Russell 1000 Value Index increased 8.23% over the same period.

{"dialogBean":{"articleAbstract":"The Atlanta Federal Reserve currently estimates real GDP growth of approximately 3.0% for Q2 2026, suggesting continued economic resilience.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"June 01, 2026","trustmarkExpirationDate":"July 28, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - June 1, 2026","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2026/6/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2026/6/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

May 1, 2026

The Atlanta Federal Reserve currently estimates real GDP growth of approximately 3.5% for Q2 2026, suggesting continued underlying economic resilience.

April 15, 2026

In March, the ISM Services PMI registered 54.0, indicating continued expansion in the services sector.