September 15, 2025

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In August, the ISM Services PMI rose to 52.0, indicating modest expansion in the services sector. The NFIB Small Business Optimism Index increased to 100.8, rising in three of the last four months. The U.S. unemployment rate rose to 4.3% in August, meeting market expectations. Notably, the unemployment rate is currently at its highest level since October 2021. The Consumer Price Index increased 0.4% in August. The 12-month inflation rate rose to 2.9%, the highest level since January 2025. Over the same month, the Producer Price Index unexpectedly decreased 0.1%, while the year-overyear rate stood at 2.6%. Consumer sentiment has declined slightly, with the University of Michigan index posting a preliminary September reading of 55.4, down from 58.2 in August. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.35% as of September 11.

Fixed Income

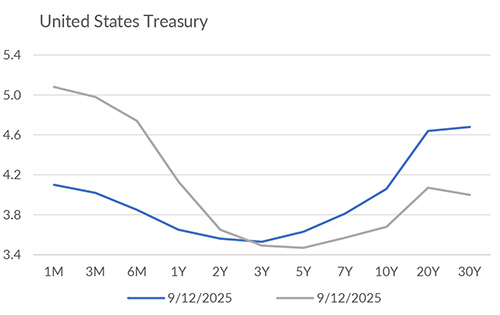

Investor attention in recent weeks has shifted from inflation to employment, with the bond market increasingly pricing in a labor-led pivot from the Federal Reserve. The next FOMC meeting is scheduled for this week, with the futures market indicating an extremely high probability of a 25 bps rate cut. The 2-year yield has declined to 3.53%, near its lowest level this year, reflecting expectations for easing. Similarly, the 10-year yield has steadily fallen over the past two months. Overall, the yield curve has steepened modestly, a reversal from the prolonged inversion seen earlier in the cycle. U.S. interest rate volatility, as measured by the ICE BofA MOVE Index, has steadily declined and currently sits at its lowest levels of the year.

Yield Curve

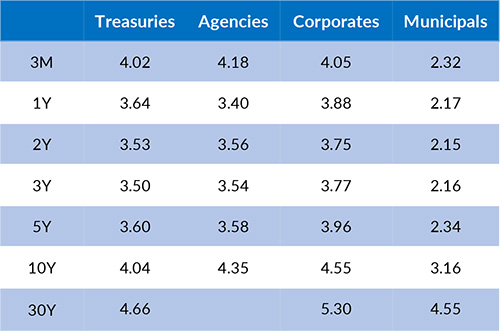

Current Generic Bond Yields

Equity

U.S. equities have continued their upward trajectory into September, with the S&P 500 up over 12% year-to-date, driven by strong corporate earnings and resilient consumer demand. Roughly 80% of S&P 500 companies beat Q2 earnings expectations. Similarly, net profit margins are near all-time highs despite ongoing tariff concerns. Since the start of August, investor sentiment has fallen, with the AAII Survey indicating a change in the share of ‘bearish’ responses from 33% to 49%. Seasonality and election-cycle models suggest a choppy market through fall, with potential for year-end upside if rate cuts materialize and trade tensions remain contained.

In 2025, the best performing U.S. sectors have been Communication Services (+24.97%), Information Technology (+17.81%), and Industrials (+15.81%). The worst performing sectors have been Health Care (+1.34%), Consumer Discretionary (+5.07%), and Energy (+5.39%). On a total return basis, the Russell 1000 Growth Index has returned 15.03% year to date, while the Russell 1000 Value Index has increased 10.58% over the same period.

{"dialogBean":{"articleAbstract":"In August, the ISM Services PMI rose to 52.0, indicating modest expansion in the services sector.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"September 15, 2025","trustmarkExpirationDate":"July 27, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - September 15, 2025","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2025/9/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2025/9/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

September 1, 2025

The U.S. Leading Economic Index declined slightly in July to 98.7, marking the eighth consecutive month with a decrease or an unchanged reading for the index.

August 15, 2025

In July, the ISM Services PMI fell slightly to 50.1, indicating neutral levels of service sector activity.

August 1, 2025

The U.S. Leading Economic Index declined to 98.8 in June, marking the sixth decline in the past seven months.