August 15, 2025

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

In July, the ISM Services PMI fell slightly to 50.1, indicating neutral levels of service sector activity. The NFIB Small Business Optimism Index rose to 100.3 in the same month, slightly above its long-run average. The unemployment rate rose slightly to 4.2% in July, with little overall change in labor market conditions. The Consumer Price Index rose by 0.2%, bringing the annual inflation rate to 2.7%. The Producer Price Index increased by 0.9%, the highest month over month change since June 2022. As a result, producer prices have risen 3.3% on an annual basis. Consumer sentiment slipped in the preliminary August reading, with the University of Michigan Index unexpectedly falling to 58.6 from 61.7 in July. The average interest rate for a 30-year fixed-rate mortgage as of August 14 was 6.58%, the lowest level since October 2024.

Fixed Income

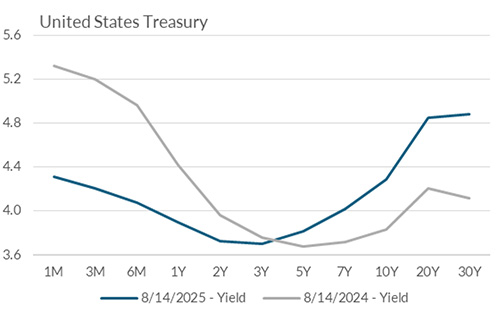

The Federal Reserve maintained the federal fund target rate at 4.25-4.50% during their most recent meeting. After a higher-than-expected July Producer Price Index reading, futures markets still indicate strong odds of a 25 bps interest rate cut in September. Likewise, markets are expecting the FOMC to deliver a total of 50 bps worth of rate cuts by the end of the year. Yields on short and intermediate bonds have stabilized, following a sharp decline near the beginning of August. Traditionally a sign of a healthy economy, the 10-year Treasury rate (4.29%) remains squarely above the 2-year rate (3.74%). All eyes now turn to Chair Powell’s remarks at the Jackson Hole Economic Policy Symposium for guidance on interest rates in the coming months.

Yield Curve

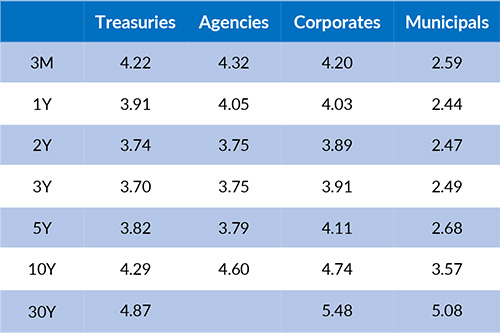

Current Generic Bond Yields

Equity

U.S. Stocks continue to make all-time highs with the S&P 500 near 6,460. The CBOE Volatility Index has continued a downward trend and now sits below 15, a sign of relatively calm markets even towards the end of Q2 earnings season. Breadth has improved, with roughly 60% of S&P 500 constituents above their 200-day average, following a period of only 45% of companies meeting that criteria in mid-June. In terms of corporate sentiment, the number of S&P 500 companies citing “recession” on their Q2 earnings calls vs Q1 declined by 87%. With most companies having reported, the Q2 earnings growth rate is approximately 11.8%, compared to previous expectations of only 4.9% as of June 30.

In 2025, the best performing U.S. sectors have been Communication Services (+17.54%), Information Technology (+16.80%), and Industrials (+15.50%). The worst performing sectors have been Health Care (-1.74%), Consumer Discretionary (1.52%), and Energy (+1.71%). On a total return basis, the Russell 1000 Growth Index has returned 12.54% year to date, while the Russell 1000 Value Index has increased 8.41% over the same period.

{"dialogBean":{"articleAbstract":"In July, the ISM Services PMI fell slightly to 50.1, indicating neutral levels of service sector activity.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"August 15, 2025","trustmarkExpirationDate":"July 28, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - August 15, 2025","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"15-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2025/8/15-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2025/8/15-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

August 1, 2025

The U.S. Leading Economic Index declined to 98.8 in June, marking the sixth decline in the past seven months.

July 15, 2025

In June, the ISM Services PMI rose to 50.8, up slightly from 49.9 in May, indicating relatively stable service sector activity.

July 1, 2025

The U.S. Leading Economic Index declined to 99.0 in May, signaling potential headwinds for future economic activity.