September 1, 2025

We use cookies on this site to improve the user experience and analyze website traffic. To learn more about how we use cookies, please see our Manage Cookies page. You can adjust your cookie settings to allow only specific types of cookies. By continuing to use our site, you are agreeing to our Privacy Policy and cookies usage.

Economic Outlook

The U.S. Leading Economic Index declined slightly in July to 98.7, marking the eighth consecutive month with a decrease or an unchanged reading for the index. The ISM Manufacturing PMI increased to 48.7 in August; however, the index indicates an ongoing contraction in the manufacturing sector. Industrial Production rose 1.4% year-over-year in July, the highest annual change since January. The University of Michigan Consumer Sentiment Index posted a final reading of 58.2 in August, down from 61.7 in July. The 5-Year Breakeven Inflation Rate stood at 2.47% as of September 1, pointing to stable medium-term inflation expectations. Capacity Utilization edged down to 77.5% in July, in line with expectations. Average hourly earnings rose 0.3% in July and 3.9% year-over-year. The NAHB Housing Market Index fell to 32 in August, remaining well below its historical average. The average interest rate for a 30-year fixed-rate mortgage was approximately 6.56% as of August 28.

Fixed Income

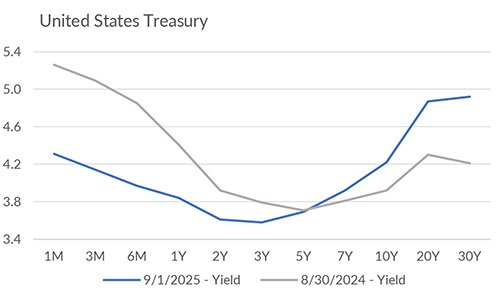

Following Chair Powell’s Jackson Hole remarks, markets now assign roughly an 85% probability of a 25 bp cut at the September 16–17 FOMC meeting. The current FOMC target rate remains at 4.25%-4.50%. The 2-year Treasury yield is near its lowest level since October 2024, as future rate cuts are priced in. Meanwhile, the 10-year Treasury yield remains rangebound, as it has traded between 4.0% and 4.6% nearly the entire calendar year. Credit conditions appear to be strong. The Moody's Seasoned Baa Corporate Bond yield relative to the 10-year Treasury yield is currently at a spread of 1.74%. Likewise, the spread between the ICE BofA US High-Yield Index yield relative to the 10-year Treasury yield sits at the lowest level on record.

Yield Curve

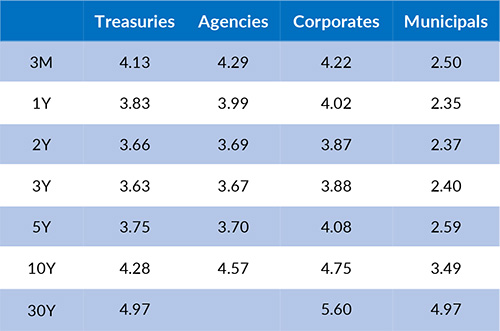

Current Generic Bond Yields

Equity

U.S. stocks remain near all-time highs with the S&P 500 trading at 6415. Breadth for the index is still strong, as roughly 62% of its stocks trade above their 200-day moving average. Earnings support remains a tailwind—about 81% of S&P 500 companies beat EPS estimates for Q2. This year, the equalweight S&P 500 index total return (+7.73%) continues to trail the market cap-weighted index total return (+9.90%).

In 2025, the best performing U.S. sectors have been Communication Services (+17.91%), Industrials (+16.12%), and Information Technology (+14.04%). The worst performing sectors have been Health Care (+0.81%), Consumer Discretionary (+2.02%), and Consumer Staples (+5.54%). On a total return basis, the Russell 1000 Growth Index has returned 11.33% year to date, while the Russell 1000 Value Index has increased 10.01% over the same period.

{"dialogBean":{"articleAbstract":"The U.S. Leading Economic Index declined slightly in July to 98.7, marking the eighth consecutive month with a decrease or an unchanged reading for the index.","priority":"1","isFeatured":"false","isNews":"false","hideInBlogLanding":"false","trustmarkDate":"September 01, 2025","trustmarkExpirationDate":"June 26, 2026","authorBean":{"authorName":"Alex Essary","profilePicPath":"/content/dam/trustmark/associates/ef/alex-essary_sm.jpg"}},"pageTitle":"Portfolio Manager Commentary - September 1, 2025","pageThumbnail":"/content/dam/trustmark/advice/commentary/Portfolio-Manager-Commentary_th.jpg","pageTags":["trustmark:investment-management"],"pageTagTitles":["Investment Management"],"pageName":"01-portfolio-manager-commentary","pagePath":"/content/trustmark/trustmark/advice/2025/9/01-portfolio-manager-commentary","externalPagePath":"https://www.trustmark.com/advice/2025/9/01-portfolio-manager-commentary.html","fbAppId":"662611918413208","positioningBean":[{"layout":"small"},{"layout":"large-horizontal"},{"layout":"large-vertical"}]}

Related Articles

August 15, 2025

In July, the ISM Services PMI fell slightly to 50.1, indicating neutral levels of service sector activity.

August 1, 2025

The U.S. Leading Economic Index declined to 98.8 in June, marking the sixth decline in the past seven months.

July 15, 2025

In June, the ISM Services PMI rose to 50.8, up slightly from 49.9 in May, indicating relatively stable service sector activity.